by AdvisorAnalyst.com in collaboration with AGF Capital Partners

Prepare, Don’t Predict: Building Resilient Portfolios with Private Credit

For decades, investors climbed the 60/40 ladder with confidence. Now, every step feels less steady. High inflation that refuses to budge, interest rates that won’t come down anytime soon, and the growing correlation between stocks and bonds are forcing investors to rethink how they build portfolios using alternatives.

And here’s where, and why, the conversation starts shifting—toward private credit. Not just as a way to hunt for yield, but as a tool to help manage risk, sidestep duration drag, and prepare for the next market surprise—whenever and however it shows up.

Ash Lawrence, Head of AGF Capital Partners, and Ryan Dunfield, CEO at SAF Group break down why private credit isn’t just timely—it might be essential.

Why the Old Portfolio Formula Is Breaking Down

The wake-up call came in 2022. As Lawrence puts it, “When interest

rates and inflation are moving in the same direction upwards, that causes stocks and bonds to operate in a more correlated fashion... I think that reinforces this conversation people are having, to rethink the 60/40 portfolio.”

Bond Markets Are Out of Sync with Reality

Dunfield gets right to the point. “Bond pricing mechanisms have

become almost broken,” he said, referring to how disjointed spot rates, long-term yields, and models have become.

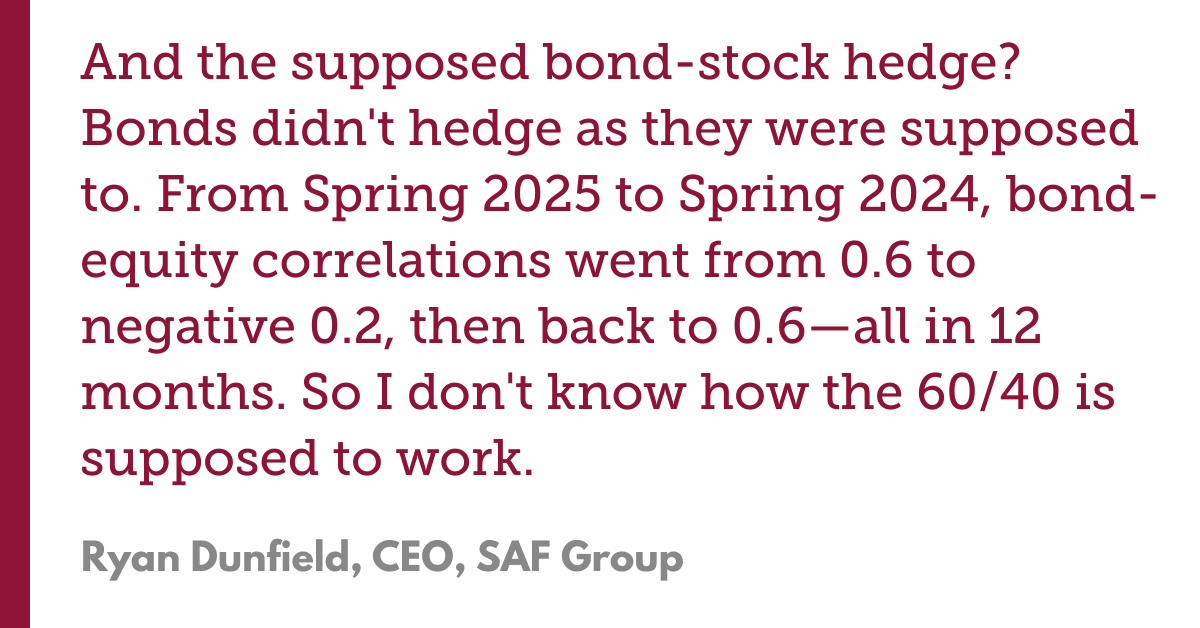

Spreads on investment-grade bonds are sitting at “late 90's levels,” which, given current macro conditions, makes little sense. And the supposed bond-stock hedge? “They didn't hedge inflation as they were supposed to,” Dunfield says. “From Spring 2025 to Spring 2024, Bond-equity correlations went from 0.6 to negative 0.2, then back to 0.6—all in 12 months.” That kind of volatility makes traditional diversification look unreliable.

His point: the relationship between stocks and bonds is not what it used to be, with correlations swinging wildly—sometimes bonds cushioned losses, other times they made them worse. That kind of volatility is making traditional diversification look less reliable.

Ash Lawrence on the nature of the 60/40 portfolio model.

How do floating rate coupons work?

Floating Rate Private Credit: Income That Rises with Rates

Floating rate private credit, on the other hand, plays by a different set of rules.

Dunfield lays it out simply: “You receive as the investor a spread on top of risk-free rate. So if risk-free rate starts to increase, you're earning a higher total coupon payment.”

That’s exactly the behaviour clients used to expect from bonds—and the kind of outcome that makes sense to them. “It’s that simple,” he says.

Lawrence adds that the SAF Group approach focuses on senior, secured private debt. “From my perspective, I view it as complementary to both equities and [traditional] fixed income strategies.”

Unlike fixed-rate bonds, floating loans reset in real-time. You’re not stuck holding yesterday’s rate. And when loans roll over? They reset at today’s rate. That keeps portfolios current—and income flowing.

The truth is, the 60/40 mix wasn’t designed for today’s world. It

thrived in a long stretch of falling rates and low inflation. That’s

over. Now, it’s time to ask: what else belongs in the mix?

Lawrence makes the case: when major indices like the S&P 500 has

“pretty big concentration” with just ten stocks making up roughly 40% of the index, and traditional bonds are struggling with rate volatility, diversification isn’t what it used to be.

Adding uncorrelated strategies—like private credit—can help restore balance.

Avoiding Duration Traps and Reinvestment Headaches

Traditional bonds lock you into yesterday’s pricing. And when they mature? You’re left reinvesting at whatever the market gives you—often less.

As Dunfield explains, “If you had picked up a series of investment grade bonds two years ago, when spreads were 175 bps...today it's 85 bps [of spread], and guess what? They're about to reverse. So you're reluctantly buying 85 bps knowing that it’s probably going to revert to mean and you're going to lose your price.”

Private credit flips that equation. You get tighter structures, stronger covenants, and floating-rate exposure. Plus, loans often come with floors—so even if rates fall, you won’t drop below a set minimum.

“We try aggressively to put those floors in place when rates are high,” says Dunfield. “And luckily in Canada... we're not competing against the CLO and rate funded markets, so we can negotiate floors that are fairly tight to spot.”

Canada’s Edge: A Less Crowded, More Nimble Market

Dunfield highlights an overlooked edge: “The Canadian market is approximately one-40th the size on the private credit side as the U.S. market.”

That might sound limiting, but [in reality] it’s actually a huge benefit. Smaller may lead to less competition, better terms, and—most importantly—more time to structure deals. “We tend to have more favourable balance as the lender...and we get to take advantage of that balance.”

“We don’t often see large, highly sophisticated investors bleeding their way up from New York into Canada for opportunities,” he says. “And with less competition, we tend to have more favourable balance as the lender in the market... more pricing power, more covenants, and time to adjudicate risk.”

There’s also a small, specialized group of domestic private lenders, especially for Canadian SMEs, and very little pressure from syndicated or public loan markets. The result? A real, workable gap that private investors can step into—and some already are.

Banks Pull Back. Private Credit Steps In.

There’s been some hand-wringing about credit shifting away from banks. Dunfield tackles that head-on.

“Banks are very highly regulated entities that are very highly levered, funded by withdrawable deposits,” he says. This isn’t a “shadow banking” story—it’s an opening. With Basel III already biting and Basel IV expected by mid-2026, Canadian banks face tougher capital buffers and may need to shed up to $270B in assets, according to Scotiabank.1 That makes mid-market lending less attractive [to them] than investment-grade credit, and is causing banks to step back.

Private credit managers, on the other hand, are generally less levered, more patient, and backed by locked-in capital. “It is moving credit into what I would call more stable hands,” he says. The result: a growing funding gap for SMEs. Private lenders are built to fill it—bringing patient capital, tighter structures, and speed where banks are constrained. For advisors and investors, this isn’t just defense against volatility; it’s a chance to participate in a structural shift in how capital gets deployed.

What to Look For in a Private Credit Manager

When it comes to picking a private credit manager, Lawrence offers three key high criteria:

- Structuring Skill: “Credit is about mitigating downside risk... that feature is vitally important, and especially in private debt.”

- Stress-Tested Track Record: “You always want [your manager] to have restructuring capabilities in their back pocket.”

- Strategy Fit: “Match the investment outcomes that you're looking for with the skillset of that manager.”

He notes that AGF has been investing with SAF Group since 2014 across multiple vehicles, including the AGF SAF Private Credit Trust, which provides access to the potential benefits of private credit that may otherwise only be available to institutional investors.

Why Governance Matters in This Partnership

Most partnerships stop at distribution. AGF and SAF went further, building a true joint venture—and it shows where it counts: governance.

Advisors know the stakes. Weak oversight has burned investors before, which is why AGF’s compliance strength and SAF’s credit expertise make this framework stand out.

Two Ways to Access the Strategy

The partnership via AGF Capital Partners offers two ways to access private credit:

- AGF SAF Private Credit Limited Partnership (LP): a pure-play structure with 100% exposure to private debt, designed for institutions and sophisticated investors comfortable with illiquidity.

- AGF SAF Private Credit Trust: tailored for investors seeking the ballast of private credit but with a liquidity sleeve, and lower minimum investments. Holding 10–15% in liquid assets, it’s built for those who need flexibility.

“Both vehicles have the same underlying portfolio,” Lawrence clarifies. “It’s just a matter of deciding on fit.”

Where the Opportunities Are Right Now

Dunfield points to some of the near-term plays SAF is targeting for the AGF SAF Private Credit strategy: mining and metals, real estate lending pools (through non-bank intermediaries), NAV loans to financial institutions (these are loans made against the net asset value of a financial institution’s portfolio of investment assets), and ABF or asset-based financing (loans made against e.g. pools of mortgages, credit card receivables, equipment loans, corporate receivables, etc.).

These aren’t deals you find on the open market. They’re bespoke, negotiated, and structured in ways that can give investors a risk-adjusted edge.

Private Credit Managers Are Worriers (And That’s a Good Thing)

When asked why now is the time to prepare for what's ahead in markets rather than predicting it, Dunfield puts it simply: "It’s not about guessing whether the ladder will hold up in the mid- to long-term period ahead—it’s about reinforcing the rungs today, so the climb stays steady no matter what.”

Ash Lawrence on the high criteria that defines manager selection, like SAF Group.

Ash Lawrence on the AGF SAF Group Partnership, and Governance..

Ash Lawrence on how and where the strategy fits in portfolios.

What is the difference between private credit and traditional bonds?

What does the public bond market look like right now?

How do you think about risk management?

Lawrence adds, “If you want to be prepared, it does feel like we're in a time period to start to rethink the portfolio and ensure proper diversification.”

The truth is, the 60/40 mix wasn’t designed for today’s world. It thrived in a long stretch of falling rates and low inflation. That’s over. Now, it’s time to ask: what else belongs in the mix?

Lawrence makes the case: when major indices like the S&P 500 have “pretty big concentration” with just ten stocks making up 40% of the index, and traditional bonds are struggling with rate volatility, diversification isn’t what it used to be.

Adding uncorrelated strategies—like private credit—can help restore balance.

Private credit flips that equation. You get tighter structures, stronger covenants, and floating-rate exposure. Plus, loans often come with floors—so even if rates fall, you won’t drop below a set minimum.

“We try aggressively to put those floors in place when rates are high,” says Dunfield. “And luckily in Canada... we're not competing against the CLO market, so we can negotiate floors that are fairly tight to spot.”

It’s built to avoid conflicts and improve decision-making.

In practice:

- Loan approvals come from a joint investment committee with both firms at the table.

- Valuations are handled independently with a third party, away from the deal team who originated the loans.

- Final valuation sign-offs sit with a committee consisting of AGF compliance, risk, and credit specialists—again, separate from the SAF loan origination team.

This separation keeps judgment objective. For advisors, it means a strong governance model for Canadian retail private credit—and a built-in safety net for clients.

“I’m a credit guy, so I’ll bring an umbrella when there’s not a cloud in the sky," he adds. "I’m worried about stagflation. I’m worried about rates plotting eerily close to the seventies and eighties, and that we're about to have another inflation period, when combining early rate cuts with tariffs. The IPO market in Canada is weak. The banks are getting more regulated. The consumer today is extremely fragile.”

Key Takeaways

As markets evolve, so too must the tools and strategies advisors use to guide their clients. Here are the key takeaways from the conversation:

- The 60/40 Portfolio Needs Reinforcement: The old mix worked in a low-rate era. With stocks and bonds now moving together, adding private credit can potentially restore balance.

- Bonds and Private Credit in Balance: Bonds remain central to portfolios, but pairing them with private credit—offering shorter duration, stronger covenants, rate floors, and competitive yields—is complementary, and may add resilience in a higher-for-longer environment.

- Canada’s Underrated Advantage: A smaller, less crowded market typically means better pricing, stronger terms, and more time to structure deals.

- Manager Quality Matters: Governance and skill take priority over performance track record when it comes to selection. AGF Capital Partners believes that structuring, crisis-tested experience, and alignment with investor goals separate the best from the rest.

Footnotes:

1 Scotiabank "Does the Federal Government Really Want Banks to Lend Less?" May 24,. 2025.

Ash Lawrence

Head of AGF Capital Partners

Ash Lawrence is Head of AGF Capital Partners, AGF Management Limited’s diversified alternatives business, and a member of AGF’s Executive Management Team. With over 20 years of expertise in alternative investments and portfolio management, Ash leads initiatives to expand AGF’s private asset and alternative strategy capabilities. His team partners with experienced investment managers, providing strategic support, resources, and capital to foster growth and innovation. Before joining AGF, Ash spent 16 years at Brookfield Asset Management, where he led Canadian real estate investments and managed portfolios across North America and Brazil. Ash holds an MBA from the Rotman School of Management and a Bachelor of Applied Science in Civil Engineering from the University of Waterloo. He serves on multiple boards and is a Global Governing Trustee for the Urban Land Institute. Ash’s early career includes financing municipal infrastructure and developing solutions for public and private sectors.

Ryan Dunfield

CEO & Managing Principal, SAF Group

Ryan Dunfield is CEO and Co-Founder of SAF Group, a private credit firm serving clients through closed-ended funds, evergreen funds, institutional platforms, and insurance solutions. Prior to founding the SAF Group, Ryan worked at an event-driven hedge fund, a Canadian private equity manager, and, earlier in his career, with a Canadian financial institution in its corporate and investment banking group. He has over 20 years experience working in credit capital markets. Ryan is originally from Vancouver, British Columbia, earned his B.A. in Economics from the University of Calgary with a minor in Commerce.

About AGF Capital Partners

AGF Capital Partners is AGF’s multi-boutique alternatives business with diverse capabilities across both private assets and alternative strategies. Clients benefit from the specialized investment expertise of Affiliate Managers combined with the organizational support and breadth of resources of AGF Management Limited (AGF).

The Affiliate Managers include SAF Group, Kensington Capital Partners and New Holland Capital which collectively manage approximately CAD$13.7 billion in assets across private equity, private credit, venture capital and absolute return strategies.

The views expressed in this article are those of the author and do not necessarily represent the opinions of AGF, its subsidiaries or any of its affiliated companies, funds or investment strategies.

This article is solely for information purposes and does not constitute an offer or solicitation of an offer or any advice or recommendation to purchase any securities or other financial instruments and may not be construed as such.

Any securities referenced in this article will only be offered and sold pursuant to a confidential offering memorandum in such Canadian jurisdictions where they may be lawfully offered for sale to eligible investors who qualify as “accredited investors” under applicable Canadian securities laws. In addition, any offer or sale of, or advice related to, any securities referenced will be made only by a dealer registered in the appropriate category or relying on an exemption from registration. No Canadian securities regulatory authority has reviewed or in any way passed upon the information contained in this article or the merits of any securities referenced.

This document may contain forward-looking information that reflects our current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein.

®/TM The “AGF” logo and all associated trademarks are registered trademarks of AGF Management Limited and used under licence.

Copyright © AdvisorAnalyst.com, AGF Capital Partners